Comprehensive illustrative guidance on preparing IFRS-compliant interim condensed consolidated financial statements for reporting periods ending in 2026. The publication demonstrates the application of IAS 34 Interim Financial Reporting and related IFRS Accounting Standards through practical examples, financial statements, disclosures, notes, and reporting considerations. It includes guidance on revenue recognition, business combinations, segment reporting, financial instruments, fair value measurement, climate-related disclosures, Pillar Two tax considerations, and emerging reporting requirements. The publication also provides an appendix covering IFRS 18 Presentation and Disclosure in Financial Statements, including transition disclosures, new presentation requirements, management-defined performance measures, and statement of cash flow amendments.

Filter insights by:

Showing 16 of 18 content results

A comprehensive guide to IFRS 15 covering Step 1 (identifying contracts), Step 2 (identifying performance obligations), and principal versus agent considerations, with practical insights on revenue recognition, control assessment, and application of the five-step model.

A concise overview of IFRS 18’s key requirements, explaining how the new IASB standard will change the presentation and disclosure of financial statements from 2027.

The IFRS Foundation has issued IFRS Alert 2025‑08, introducing new illustrative examples to help entities apply existing disclosure requirements related to uncertainties in financial statements. The publication provides practical insights to support transparent reporting, enhance consistency in application, and improve the quality of financial disclosures under IFRS Accounting Standards. This alert highlights key expectations for preparers, auditors, and stakeholders focusing on areas of estimation uncertainty, judgments, and risk‑sensitive disclosures.

Grant Thornton’s publication “Navigating the Changes to IFRS 2026” provides a comprehensive and practical overview of all IFRS Accounting Standard changes issued between 1 January 2025 and 31 December 2025. It outlines new standards, amendments to existing IFRS requirements, interpretations, and effective dates relevant to 2025–2026 year‑ends. The guide includes commercial impact assessments, early‑adoption considerations, and disclosure requirements under IAS 8, making it a valuable resource for financial statement preparers, auditors, and accounting professionals.

ISSB amendments to IFRS S2 introduce targeted reliefs to greenhouse gas emissions disclosures, including Scope 3 financed emissions, jurisdictional measurement requirements, and industry classification flexibility, effective from 1 January 2027.

IFRS Example Consolidated Financial Statements 2025 Comprehensive guide illustrating IFRS-compliant consolidated financial statements for Illustrative Corporation Group as of 31 Dec 2025. Covers profit or loss, OCI, financial position, equity changes, cash flows, and detailed notes on accounting policies, climate-related disclosures, economic uncertainty, segment reporting, revenue recognition, financial instruments, and risk management. Includes updates on new standards (IFRS 18, IFRS 19), sustainability reporting, impairment testing, acquisitions/disposals, and liquidity monitoring. Designed to support consistent internal and external reporting with emphasis on materiality, transparency, and entity-specific application.

The International Accounting Standards Board (IASB) has issued a revised ‘Practice Statement 1 Management Commentary’ (the Practice Statement). The objective of the revision is to provide a global benchmark for the preparation of management commentary accompanying financial statements including sustainability-related financial disclosures. The Practice Statement achieves this by adopting an objectives-based framework, focusing on what investors need to enable them to assess an entity’s ability to create value and generate cash flows over time. The Practice Statement is non-mandatory but designed to be used alongside IFRS Accounting Standards and IFRS Sustainability Disclosure Standards.

IFRS for SMEs - IASB issues a major update in a third edition of this Accounting Standard

This publication is designed to give preparers and reviewers of IFRS financial statements a high-level awareness of recent changes to International Financial Reporting Standards.

The 2024 edition of the publication has been updated for changes to International Financial Reporting Standards (IFRS) that were published between 1 January 2023 and 31 December 2023. The publication now covers 31 March 2023, 30 June 2023, 30 September 2023, 31 December 2023 and 31 March 2024 financial year ends.

The 2023 edition of the publication has been updated for changes to International Financial Reporting Standards (IFRS) that were published between 1 January 2022 and 31 December 2022.

The 2022 edition of the publication has been updated for changes to International Financial Reporting Standards (IFRS) that were published between 1 January 2021 and 31 December 2021. The publication now covers 31 March 2021, 30 June 2021, 30 September 2021, 31 December 2021 and 31 March 2022 financial year ends.

Navigating the changes to International Financial Reporting Standards (2021 edition)

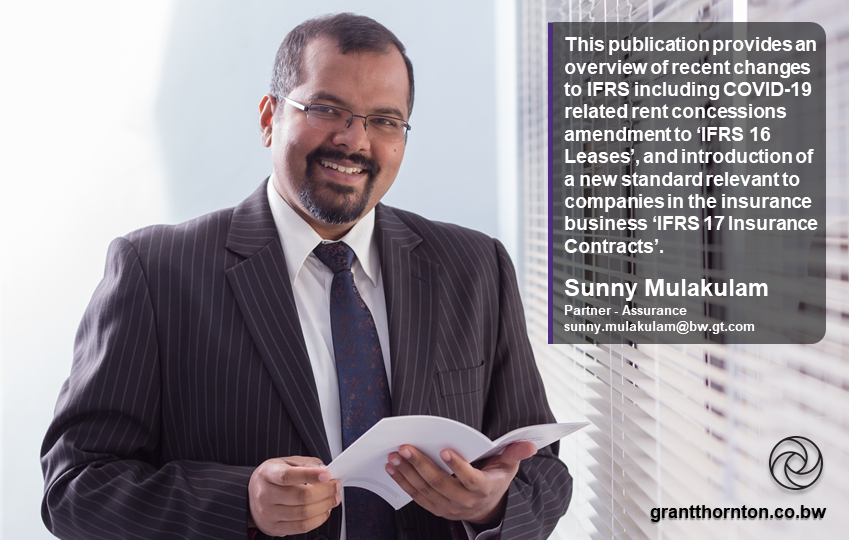

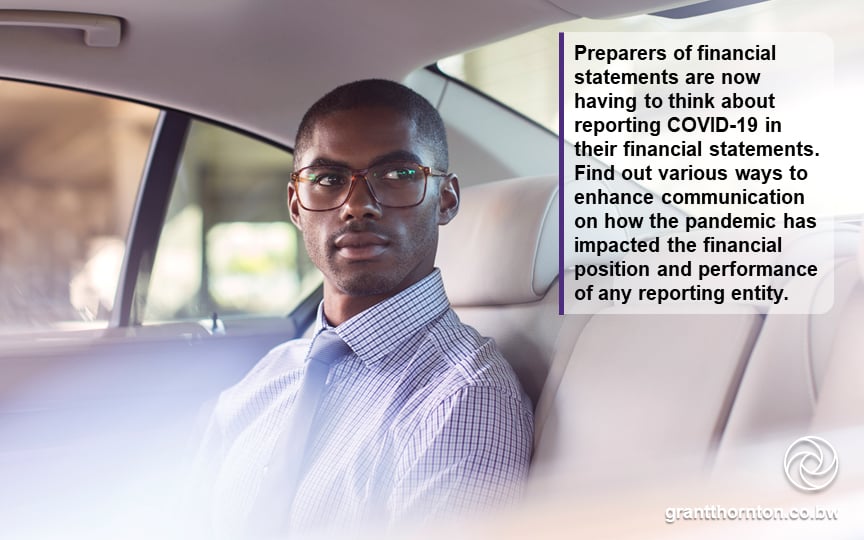

COVID-19 Financial Reporting and Disclosures